Holy Trinity Catholic School Division’s finance department has spent much of the summer re-imagining how the division manages its surplus and reserve accounts and how adding a new contingency reserve fund could look.

Chief Financial Officer (CFO) Curt Van Parys presented a detailed report to trustees during their August board meeting about the proposed changes and how the updates would affect reporting of accounting activities.

His document included spreadsheets with a historical overview of Holy Trinity’s surplus/reserve position and before and after comparisons showing the implications of adopting a contingency reserve. He also recommended eliminating many small reserve accounts since they are unmanageable.

The proposed changes will likely be introduced in the 2020-21 audited financial statement report. The contingency reserve proposal would be used for board election costs, capital expenses for buildings, technology and transportation, and unforeseen expenses or revenue decreases.

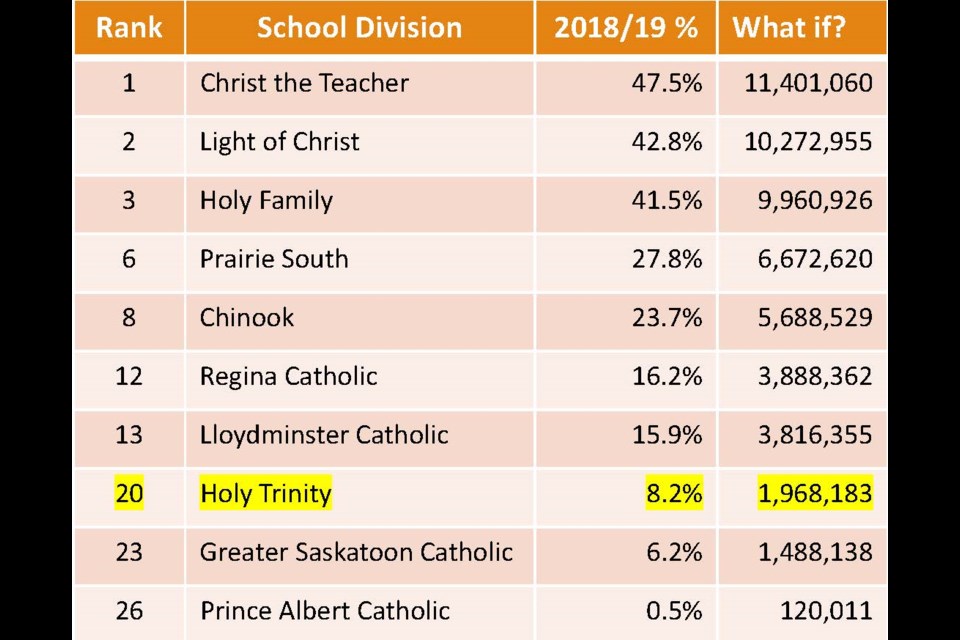

The genesis for this project arose after the Saskatchewan Association of School Business Officials (SASBO) produced a report that looked at the discretionary reserves and restricted amounts of all 27 school divisions in the 2018-19 school year, Van Parys explained. SASBO’s report also reviewed what percentage the discretionary reserves represented in the overall operational revenues picture.

For Holy Trinity, its discretionary reserves in 2018-19 were $1.96 million, representing 8.16 per cent of total revenues. In 2019-20, its discretionary reserves were $3.6 million, representing 13.48 per cent of total revenues.

The total amount of accumulated surplus in 2018-19 excluding capital grants was $24.1 million.

Van Parys thought the SASBO report was an “excellent” document that the Holy Trinity board and division administration should see since it could help them learn how other divisions manage their surplus/reserve position.

“I’m not advocating … that the school division or the board make decisions just for the express purpose of improving our financial position. We’ve got a relatively healthy reserve/surplus position … ,” he said. “What I am recommending in the future is I think there is an opportunity there to learn from school divisions that have better surplus reserve positions than us.”

The SASBO report placed Holy Trinity 20th for discretionary reserves as a percentage of total revenues at 8.2 per cent ($1.96 million). In comparison, Prairie South School Division was sixth at 27.8 per cent ($6.6 million), and Christ the Teacher in Yorkton was first at 47.5 per cent ($11.4 million).

During the board meeting, Van Parys laid out some of the purposes that operational reserve accounts serve. These include addressing cashflow changes, minimizing the use of lines of credit, addressing revenue fluctuations, facilitating long-term planning and multi-year budgeting, funding non-school capital purchases, and funding renewal of the bus fleet, curriculum and IT.

Other purposes include supporting building infrastructure capital project shortfalls, supplementing school-focused Preventative Maintenance and Renewal funding, acting as a placeholder for third-party grants, and funding cyclical expenses such as election costs.

Meanwhile, Van Parys’ proposed changes would reduce the number of “other” reserve accounts over time. For example, there was one such account in 2009-10, while there were 17 in 2019-20.

“We have too many,” he said.

Van Parys also proposed re-designating the unrestricted surplus to a restricted or designated purpose since eliminating it might send the wrong message to the public. A large portion of the unrestricted account would also go into the contingency reserve, along with unused government grants, the Vanier Collegiate building renewal reserve, and the transportation and technology reserves.

In particular, Van Parys raised concerns about two accounts: school-generated funds and professional development (PD) money. Both are risky to address, he said, since the former requires a long-term change in budgetary practices while the latter requires a negotiated change to the local teachers’ union contract.

There was $79,000 in the union’s PD account in 2010-11, while that number is now around $300,000, he added. So, the way to curtail this growth is to cap it at a percentage of PD funding.

The next Holy Trinity board meeting is Monday, Sept. 20.